Dollar On Thin Ice As Three Forces Hit: Risk Rally, Central Bank Divergence, Yen Shock

Dollar’s broader weakness reasserted itself last week, even as it managed a modest late rebound against Euro. Across the board, however, the greenback remains under pressure, with underlying momentum and sentiment pointing to further downside ahead. Technically and fundamentally, Dollar is now skating on thin ice, with recent price action suggesting the near-term rebound has already run its course.

The weakness is not driven by a single catalyst but rather a convergence of forces that are reshaping global markets. Strong risk-on sentiment has reduced demand for safe-haven assets. At the same time, shifting central bank dynamics are eroding Dollar’s advantage. Adding to these, a sharp and unexpected reversal in Japanese Yen has acted as a powerful trigger, accelerating repositioning and amplifying downside pressure on the greenback.

Taken together, these three drivers—equity market strength, policy divergence, and Yen intervention—are creating a powerful combination. What stands out is not just the presence of these factors, but their alignment.

AI-Led Earnings Surge Drives Risk Rally to Record Highs

Risk-on sentiment was the dominant force in markets last week, with US equities extending their rally to fresh record highs. Both S&P 500 and NASDAQ closed the week strongly, capping what turned out to be their best monthly performances since 2020. Even the more cyclical DOW posted its strongest gain since November 2024, underscoring the breadth of the move.

The rally was driven by a powerful earnings season that decisively beat expectations. Analysts had entered the quarter concerned that elevated interest rates and rising energy costs would compress corporate margins. Instead, results showed that companies have been able to maintain pricing power and manage costs effectively, reinforcing confidence in the resilience of the US economy.

Technology stocks, particularly those linked to artificial intelligence, remained at the center of the advance. Alphabet and Microsoft delivered strong results, highlighting that massive investments in AI are now translating into tangible revenue growth. Cloud and enterprise services showed particularly strong momentum, confirming that the AI theme is evolving beyond early-stage infrastructure spending into real-world implementation and monetization.

Perhaps most importantly, this equity strength persisted despite ongoing geopolitical tensions. Markets largely shrugged off the risks surrounding the Middle East conflict, with traders appearing increasingly desensitized to headlines. Instead, the focus remained firmly on growth prospects and earnings momentum. As long as this dynamic holds, risk appetite is likely to stay elevated, continuing to weigh on the Dollar and shape broader market direction.

Technically, the long term up trend in equities remains firmly intact, with both S&P 500 and NASDAQ maintaining strong bullish structures. The recent breakout to record highs reinforces the view that the current uptrend is not yet exhausted, especially as pullbacks remain shallow and well-supported.

For S&P 500, near-term outlook stays bullish as long as 7,046.55 support holds. The next upside target is 61.8% projection of 4,835.04 to 6,902.34 from 6,316.91 at 7,605.63 .

A similar structure is seen in NASDAQ. As long as 24,199.00 support holds, the current uptrend is expected to extend toward 61.8% projection of 14,784.03 to 24,019.99 from 20,690.25 at 26,398.07.

Hawkish Convergence Outside Fed Pressures Dollar

A key driver behind Dollar weakness last week was the shifting outlook of global monetary policy.

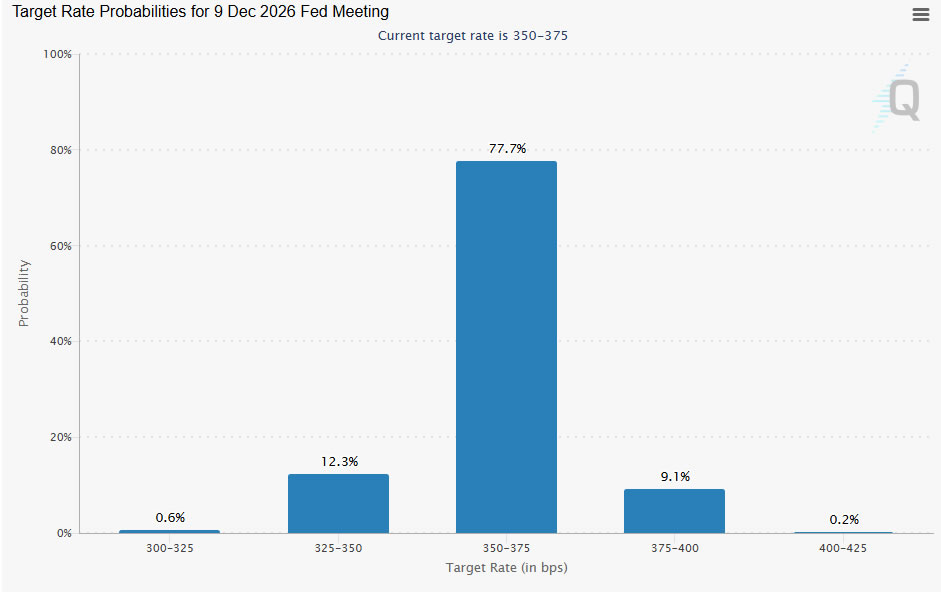

For the Federal Reserve, the decision to hold rates at 3.50%–3.75% was widely expected, but the internal dynamics were anything but calm. The meeting saw four dissents—the highest since 1992—with three regional presidents (Hammack, Kashkari, and Logan) opposing the inclusion of an easing bias in the statement. This reflects growing concern within the Committee that inflation risks remain elevated and that policy may not yet be restrictive enough.

Despite this hawkish dissent, the broader message from the Fed remains one of patience. With rates mildly restrictive at 3.50-3.75%, there is no urgency to tighten further. Market pricing reflects this balance, with around a 77% probability that rates will remain unchanged through year-end. Expectations for a rate cut have dropped sharply to roughly 12%. The Fed is no longer the most hawkish player—only that it is also not ready to ease.

The Bank of England, by contrast, is tilting more clearly toward tightening. The April 30 decision to hold at 3.75% came with an 8–1 vote split, with Chief Economist Huw Pill dissenting in favor of an immediate 25bps hike. His position highlights growing concern about persistent inflation, particularly from energy-driven cost pressures and the risk of second-round effects.

Markets have taken this signal seriously. Pricing for a June rate hike has settled around 60%, after jumping to 70% just after the rate announcement. Total tightening expectations stand at roughly 65bps for the year. Even as the BoE acknowledges fragile growth conditions, the bias is shifting toward further tightening,.

The European Central Bank is also moving closer to action. While it held its deposit rate at 2.00%, President Christine Lagarde’s neutral tone was quickly overshadowed by reports that policymakers are preparing for a June hike if energy prices remain elevated. The ECB is seen as “patiently waiting” rather than firmly on hold.

This shift is being driven by inflation dynamics. The jump in April CPI to 3.0%, combined with Lagarde’s acknowledgment that the Eurozone is moving toward the “adverse scenario,” has pushed markets to price in a 90% probability of a June hike. Expectations now extend to three 25bps increases by the end of 2026, targeting a terminal rate of 2.75%.

Perhaps the most dramatic shift is taking place in Japan. The Bank of Japan’s 6–3 vote on April 28 marked a significant departure from its historically unified stance. The three dissenters—Nakagawa, Takata, and Tamura—pushed for an immediate hike to 1.00%, arguing that the central bank risks falling behind the curve as inflation pressures build.

This internal split was reinforced by a sharp upward revision in the 2026 inflation forecast to 2.8%, a level well above the traditional target range. Market expectations have adjusted rapidly, with the probability of a June rate hike rising to around 74%. July remains a fallback option, particularly if geopolitical risks intensify and threaten growth.

Taken together, these developments highlight a clear convergence in global policy tightening. While the Fed remains on hold, others are catching up or even overtaking in terms of hawkish bias. This narrowing of rate differentials is a key structural driver of Dollar weakness, and unless the Fed reasserts its leadership, the pressure on the greenback is likely to persist.

Intervention Shock Triggers Yen Surge

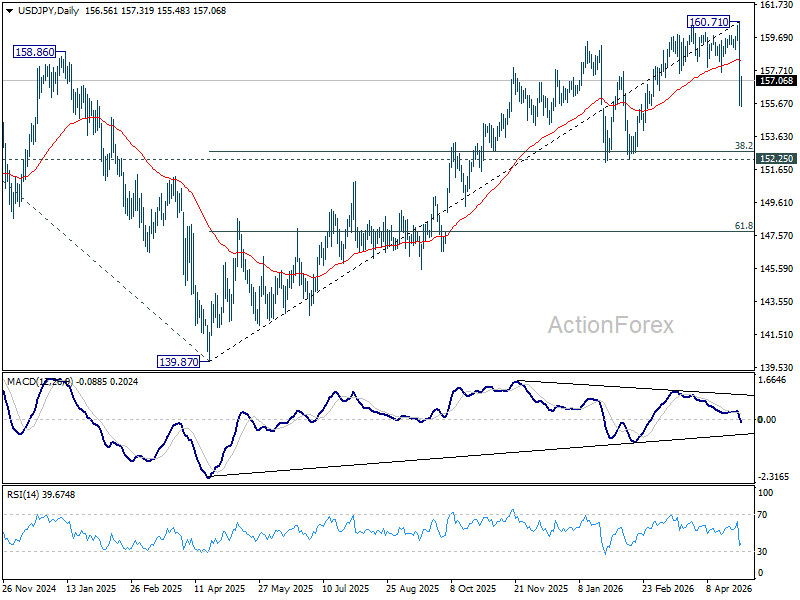

The most dramatic development in FX markets last week was the sudden and forceful reversal in Japanese Yen. After USD/JPY breached the critical 160 “red line”, Japanese authorities drew a clear line in the sand. What followed was a sharp and aggressive move that caught markets off guard and triggered a broad reassessment of positioning.

Intervention appears to have been decisive. Estimates suggest that more than USD 30 billion was deployed across April 30 and May 1, with reports from Nikkei citing Bank of Japan data indicating roughly JPY5 trillion (USD 32 billion) in Yen-buying operations. The scale of the move underlines the authorities’ determination to halt speculative excess and restore stability to the currency.

The impact was immediate and far-reaching. Yen surged around 2.2%, driving USD/JPY down toward the 156 area. More importantly, the move forced a rapid unwind of crowded carry trades, amplifying the effect beyond the Yen itself. Dollar, already under pressure from other factors, faced additional downside as positions were liquidated across the board.

This episode was not just about price action—it was a warning shot. The intervention effectively reintroduced two-way risk into what had become a one-sided market. Traders who had been comfortable pushing USD/JPY higher were forced to reassess, and opportunistic buying of Yen emerged as markets began to test how far authorities are willing to defend the currency.

Technically, the sharp fall from 160.71 suggests that a medium-term top should have been formed, reinforced by bearish divergence on D MACD. Nevertheless, the subsequent decline is now viewed as a correction of the broader uptrend from 139.87, rather than a full reversal—at least for now.

Near-term risks point to a deeper pullback toward the 152.25–152.74 cluster support zone (38.2% retracement of 139.87 to 160.71 at 152.74). . Strong support is expected in this area, which should contain downside and allow for a rebound. In the meantime, USD/JPY is likely to consolidate within a broad 152–160 range, with future direction dependent on both policy developments and global risk dynamics.

DXY Bearish Bias Remains Intact for Retesting 95.55 Low

Dollar Index’s recovery last week did little to alter the broader bearish outlook. The rebound from 95.55 should have completed at 100.64, falling short of 38.2% retracement of 110.17 to 95.55 at 101.13. This failure to sustain gains reinforces the view that the move higher was corrective rather than the start of a new trend.

The rejection at key technical levels adds weight to this interpretation. Notably, DXY was turned back below both the 101.13 Fibonacci resistance and 55 W EMA, currently around 99.49. These levels have acted as a firm ceiling, keeping the medium-term bias tilted to the downside and signaling that sellers remain in control.

In the near term, the focus shifts to 97.63 support. Decisive break below this level would confirm the resumption of the decline from 100.64 and open the way for a retest of 95.55 low.

That said, downside momentum has not yet fully accelerated. While the bias remains bearish, the current pace of decline does not yet signal an imminent breakdown. Markets may require additional catalysts—such as further policy divergence or sustained risk-on flows—to trigger a more decisive decline through 95.55.

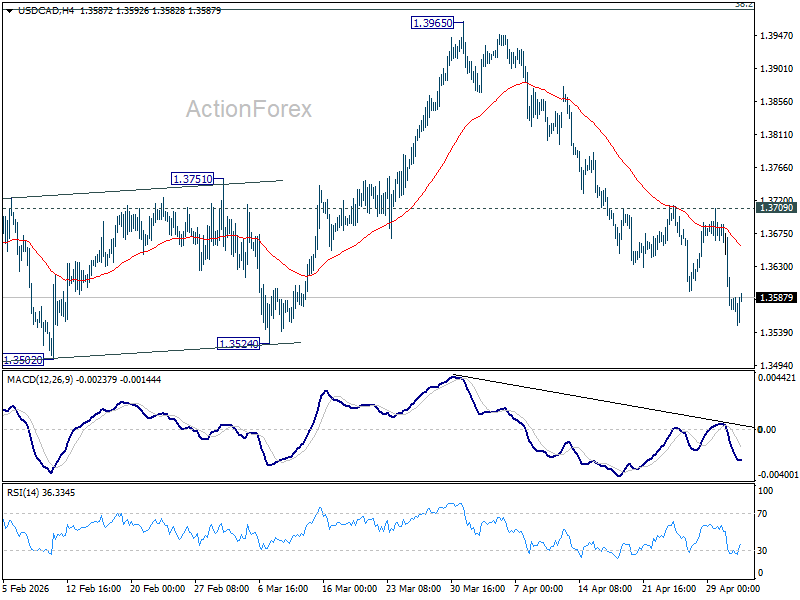

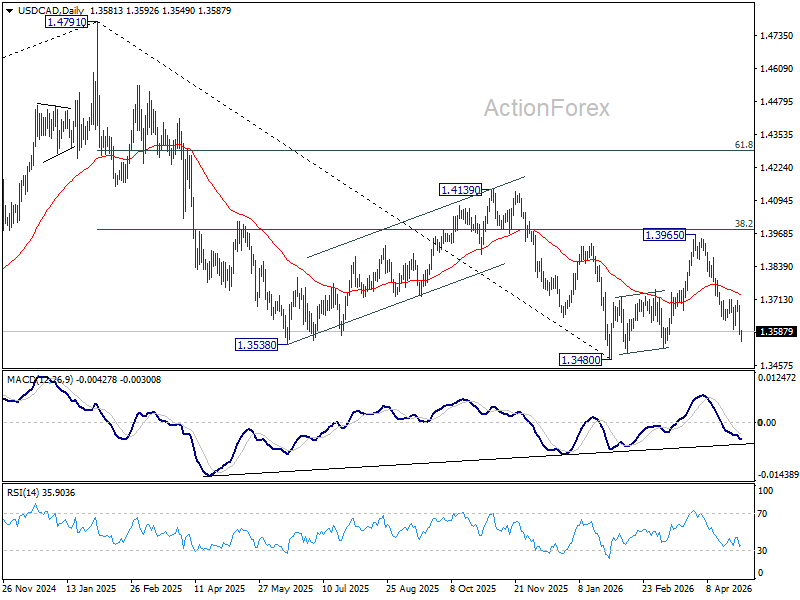

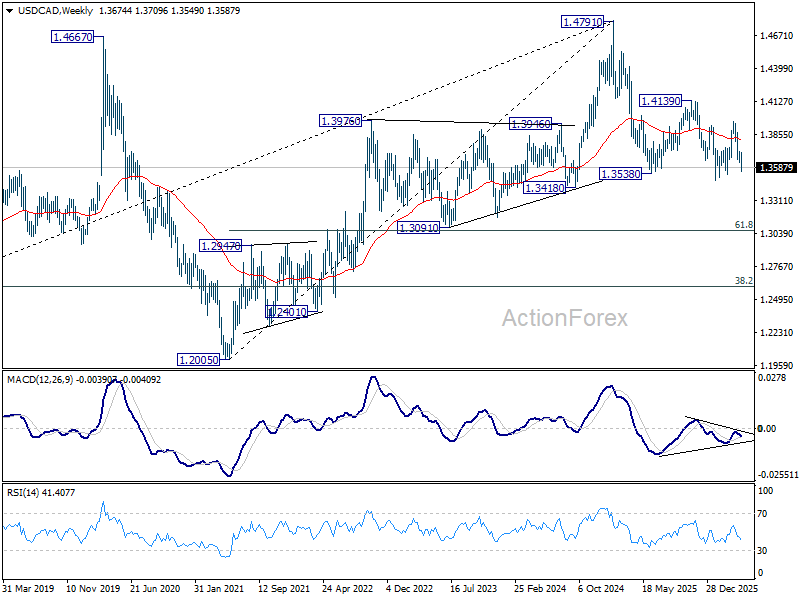

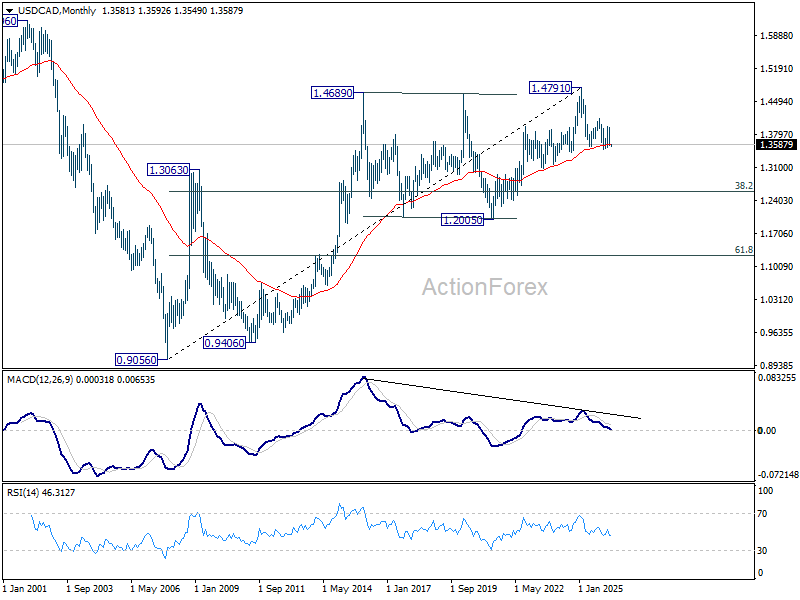

USD/CAD’s fall from 1.3965 continued last week after brief recovery. Initial bias stays on the downside this week for retesting 1.3480 low. Decisive break there will resume whole down trend from 1.4791. For now, risk will remain on the downside as long as 1.3709 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

In the long term picture, rising 55 M EMA (now at 1.3581) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more