Dollar Firm As Iran Tensions Lift Oil, Markets Turn Cautious

Dollar remained generally firm in otherwise quiet Asian trading, with broader FX flows subdued but sentiment increasingly cautious. There is a noticeable sense of nervousness across markets as geopolitical risks intensify. Precious metals edged higher, with Gold and Silver ticking up modestly. However, there is no clear follow-through buying. The lack of sustained momentum suggests traders are hedging selectively rather than positioning aggressively for full-scale escalation.

The central question is whether the US will move forward with a military strike against Iran or whether diplomatic efforts will cool the situation. Markets appear to be in wait-and-see mode. Oil, by contrast, is reacting more decisively. WTI surged above 67 and reached its highest level since last August.

US President Donald Trump overnight said he would decide “over the next probably 10 days” whether to strike Iran, adding that failure to reach a meaningful deal could lead to “bad things.” The timeline has effectively placed a geopolitical clock on markets. While Iranian and US negotiators reportedly agreed on “guiding principles,” White House officials indicated that significant differences remain. That gap is keeping energy markets on edge.

Oil traders are particularly concerned about the Strait of Hormuz, a critical chokepoint for global crude flows. Any disruption there could have outsized impact on energy prices and inflation expectations. For now, the reaction is concentrated in energy markets rather than broad risk-off flows. Equities are holding up, and haven demand in metals remains tentative.

On the weekly scoreboard, Dollar remains the strongest performer, followed by Aussie and Loonie, the latter supported by higher oil. Yen is weakest despite rising geopolitical tension, trailed by Sterling and Swiss Franc. Euro and Kiwi sit mid-pack as markets brace for the next development.

In Asia, Nikkei fell -1.12%. Hong Kong HSI is down -0.81%. China is still on holiday. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield fell -0.003 to 2.112. Overnight, DOW fell -0.54%. S&P 500 fell -0.28%. NADAQ fell -031%. 10-year yield fell -0.004 to 4.075.

UK retail sales surge 1.8% in January, strongest since May 2024

UK retail sales volumes jumped 1.8% mom in January, far exceeding expectations of 0.2% and marking the largest monthly increase since May 2024. The rebound suggests consumers began the year on firmer footing despite broader concerns over slowing growth.

On an annual basis, sales volumes rose 4.5% yoy, pointing to solid underlying demand. Over the three months to January, volumes edged up 0.1% compared with the prior three-month period and were 2.6% higher than a year earlier, indicating steady momentum rather than a one-off spike.

The data offer a counterbalance to recent signs of labor market softening and cooling inflation. While markets continue to price a March rate cut from BoE, resilient consumer spending may temper expectations for an aggressive easing cycle, particularly if inflation remains sticky in services.

Japan’s CPI slows to 1.5% in January, core measures ease further

Japan’s headline CPI slowed to 1.5% yoy in January from 2.1%, falling below the BoJ’s 2% target for the first time in 45 months. Core CPI (excluding fresh food) declined to 2.0% from 2.4%, while core-core inflation eased to 2.6% from 2.9%, signaling broader moderation in underlying price pressures.

The slowdown was largely driven by energy, where costs dropped -5.2% yoy after a -3.1% fall in December. Goods inflation cooled sharply from 2.7% to 1.6%. In contrast, services inflation remained steady at 1.4%, suggesting domestic wage-driven price gains have yet to accelerate meaningfully.

Food inflation remains elevated but is gradually cooling. Prices excluding fresh items rose 6.2% yoy, down from 6.7%. Rice inflation slowed for an eighth consecutive month to 27.9%.

Japan PMI composite jumps to 53.8, export demand surges

Japan’s private sector gathered further momentum in February, with PMI Manufacturing rising from 51.5 to 52.8 and PMI Services edging up to 53.8. PMI Composite climbed from 53.1 to 53.8, marking the strongest expansion since May 2023 and signaling a more broad-based recovery.

According to S&P Global’s Annabel Fiddes, the upturn was supported by firmer demand both domestically and overseas. Total new orders expanded at the quickest pace since May 2023, while manufacturers recorded the strongest increase in export work in eight years.

Stronger sales pushed capacity utilization higher, with backlogs rising at a record pace. Firms responded by increasing hiring, while improved demand allowed businesses to regain some pricing power despite persistent cost pressures. Business confidence also strengthened, supported by new product launches, technology demand and optimism following Prime Minister Sanae Takaichi’s landslide election victory.

Australia PMI composite dives to 52.0 in February, cost pressures reaccelerate

Australia’s February flash PMIs signaled a slowdown in private sector momentum. PMI Manufacturing slipped from 52.3 to 51.5, while PMI Services dropped sharply from 56.3 to 52.2. As a result, PMI Composite fell from 55.7 to 52.0, indicating growth continued but at a much more modest pace.

According to S&P Global’s Eleanor Dennison, the private sector was unable to sustain the strong start to the year. Both manufacturing and services recorded softer expansions in output and new orders, with the services sector experiencing the more pronounced pullback.

However, inflationary pressures remain evident. Firms reported elevated wage burdens and higher supplier costs, pushing both input and output price inflation to five-month highs. Despite softer new business growth, job creation accelerated to an 11-month high, underscoring labor market tightness.

RBNZ’s Breman confident inflation will return to target, policy not on preset path

RBNZ Governor Anna Breman said in speech that the central bank remains confident inflation will return to target despite its current 3.1% reading. She expects inflation to move back inside the 1–3% band in the first quarter and ease toward the 2% midpoint over the 12 months. That formed a key basis for the decision to keep the OCR unchanged at 2.25% this week.

Breman stressed that policymakers needed to determine whether the recent uptick in inflation signaled broader price pressures or merely a “temporary bump”. She pointed to global factors lifting tradables prices, while non-tradables inflation continues to decline, albeit slowly.

The economy expanded in the September quarter and indicators suggest recovery is continuing into early 2026. With unemployment still elevated and wage growth subdued, the RBNZ sees room for recovery without reigniting inflation.

At the same time, she reiterated that monetary policy is “not on a preset course”.

NZ trade deficit at NZD -519m as China flows diverge

New Zealand’s goods exports rose 2.6% yoy in January to NZD 6.2B, up NZD 157m from a year earlier. Goods imports increased 1.9% yoy to NZD 6.7B, up NZD 126m. The result was a monthly trade deficit of NZD -519m.

By destination, export performance was mixed. Shipments to China, New Zealand’s largest trading partner, fell NZD -118m (-7.0%) yoy. In contrast, exports to Australia jumped NZD 134M (+20%), while flows to the EU (+16%) and Japan (+11%) also posted solid gains. Exports to the US were broadly flat.

On the import side, China led the increase, with imports surging NZD 346m (+24%) yoy. South Korea also recorded a strong rise (+36%), while imports from the EU edged higher. Meanwhile, purchases from the US (-17%) and Australia (-8.1%) declined.

The data suggest stable overall trade volumes but highlight shifting bilateral flows, particularly with China, which may have implications for growth in coming months.

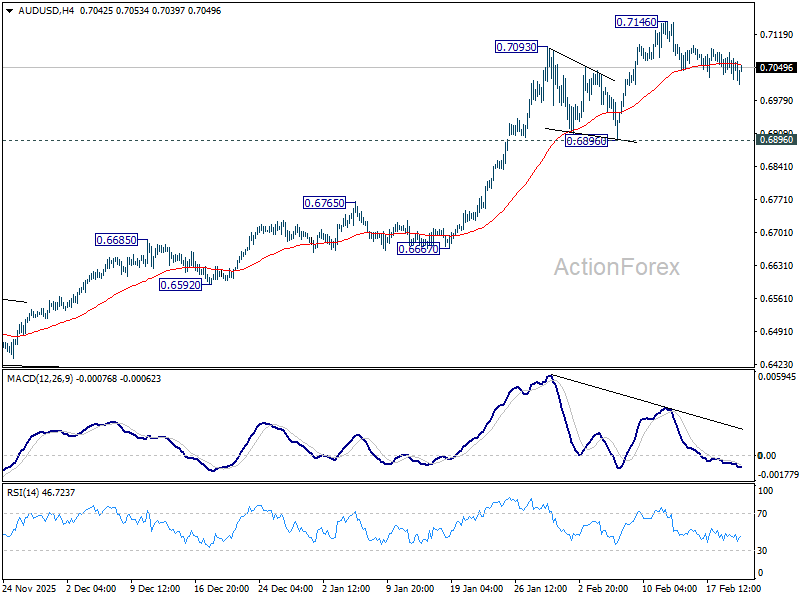

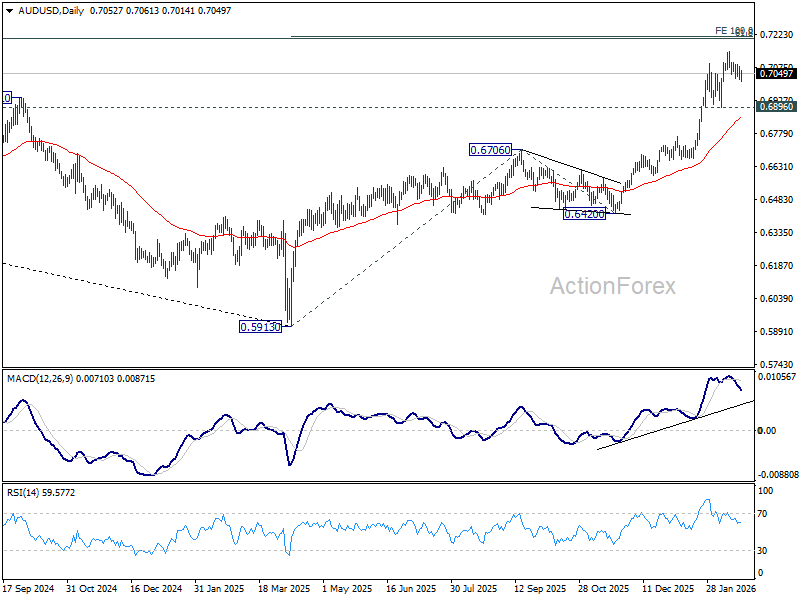

AUD/USD Daily Report

Daily Pivots: (S1) 0.7029; (P) 0.7054; (R1) 0.7085; More...

AUD/USD edges lower today as correction from 0.7146 extends, and intraday bias remains neutral. Deeper retreat might be seen, but downside should be contained above 0.6896 support to bring another rally. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more