Dollar’s selloff extended overnight, breaking to fresh lows against Euro and Swiss Franc, as markets grow increasingly uneasy about U.S. trade policy ahead of the July 9 deadline. While US equities remain resilient, with the S&P 500 and NASDAQ surging to record highs, FX markets are telling a different story, with safe haven flows driving gains in Swiss Franc and Japanese Yen.

US Treasury Secretary Scott Bessent signaled that Washington is prepared to slap higher tariffs on countries failing to reach a deal by next week. The temporary 10% rate is set to expire, potentially reverting to levels as high as 50% announced in April. President Donal Trump has also intensified his rhetoric. In a social media post, he criticized Japan for refusing to import US-grown rice, calling it a symptom of trade partners becoming “spoiled” at the US’s expense. White House spokesperson Karoline Leavitt added that countries unwilling to negotiate “in good faith” would face the full weight of US trade measures.

European leaders are pushing back. French President Emmanuel Macron called the current tariff strategy a form of “blackmail,” arguing that trade tools should promote fairness rather than coercion. He also criticized the US for simultaneously demanding more European defense spending while launching a trade war.

In the currency markets, Dollar is the weakest performer so far this week, followed by Sterling and Loonie. Swiss Franc continues to outperform as a safe haven, leading gains ahead of Yen and Kiwi. Euro and Aussie are trading in the middle of the pack.

Technically, GBP/CHF finally broke out of consolidations this week and resumed the fall from 1.1200. Near term outlook will now stay bearish as long as 1.1017 resistance holds. Sustained break of 61.8% retracement of 1.0610 to 1.1200 at 1.0835 will raise the chance of larger down trend resumption, and target 1.0610 low next.

In Asia, Nikkei closed down -1.42%. Hong Kong is on holiday. China Shanghai SSE is up 0.38%. Singapore Strait Times is up 0.76%. Japan 10-year JGB yield fell -0.039 to 1.397. Overnight, DOW rose 0.63%. S&P 500 rose 0.52%. NASDAQ rose 0.47%. 10-year yield fell -0.053 to 4.230.

Looking ahead, Eurozone CPI flash is the main focus in European session. Eurozone PMI manufacturing final, Germany unemployment and UK PMI manufacturing final will also be released. Later in the day, US ISM manufacturing will take center stage.

BoJ Tankan signals resilience, keeps 2025 hike option alive

Japan’s Q2 Tankan survey showed business sentiment holding firm despite intensifying trade tensions. While today’s Tankan beat won’t trigger immediate action, it keeps the door open for a BoJ hike policy shift before year-end, especially if trade risks stabilize.

Large manufacturers posted a headline index of +13, beating expectations of 10, and reaching the highest level since December 2024. Their forward outlook for September came in at +12, also topping forecasts of 9. The services side was more mixed. Large non-manufacturers remained steady at +34, meeting expectations, but this marked a softening from prior readings, with the September outlook dipping to +27.

Still, capital expenditure plans surprised to the upside: large firms projected FY2025/26 capex to rise 11.5% (vs. 10.0% expected), while small firms were slightly less pessimistic than forecast. The investment data points to continued confidence in the domestic recovery.

Inflation expectations remained broadly stable. Firms anticipate CPI to rise 2.4% over both one-year and three-year horizons—unchanged to slightly lower from the previous survey.

Japan’s PMI manufacturing finalized at 50.1, demand still fragile

Japan’s Manufacturing PMI was finalized at 50.1 in June, rising from 49.4 in May. While production and employment ticked higher, underlying demand remained weak.

According to S&P Global’s Annabel Fiddes, firms reported continued declines in both domestic and overseas sales, reflecting the lingering impact of global uncertainty—particularly around US tariff policy.

Despite soft demand, business sentiment improved, encouraging firms to boost output and hiring. However, Fiddes emphasized that a “renewed and sustained improvement in customer demand” is still needed to drive a broader recovery.

Price pressures also “picked up slightly”, with both input costs and selling prices rising above their long-term averages, suggesting inflationary risks remain embedded in supply chains.

China Caixin PMI manufacturing rises to 50.4, but optimism fades

China’s Caixin PMI Manufacturing rose to 50.4 in June from 48.3, topping expectations of 49.0 and marking a return to expansion territory. However, Wang Zhe of Caixin Insight cautioned that job losses persisted, external demand remained weak, and price pressures were subdued.

While the latest figures point to near-term stabilization, underlying risks remain elevated. Wang stressed that domestic demand has yet to see a fundamental turnaround and that businesses have grown less optimistic. With logistics and purchasing activity still soft, and global uncertainty intensifying, the sustainability of June’s rebound remains in question unless further policy support or demand recovery materializes.

NZIER survey shows NZ business confidence rising, inflation pressures easing

New Zealand business confidence improved modestly in Q2, with a net 22% of firms expecting better conditions ahead, up from 19% in Q1, according to NZIER’s quarterly survey.

Inflationary pressure appears to be cooling. 1% of firms reported price cuts in Q2, a sharp turnaround from the 8% that raised prices in Q1.

The report pointed to a continued “divergence between firms experiencing weak demand and firms expecting a recovery in demand”, underlining an uneven domestic outlook despite improved sentiment.

NZIER said the effect of interest rate cuts since last August has yet to fully feed through to real activity, despite supporting sentiment.

Fed’s Goolsbee dismisses stagflation risk, but warns on dual deterioration

Chicago Fed President Austan Goolsbee downplayed the risk of a 1970s-style stagflation scenario. He noted that with unemployment near 4% and inflation around 2.5% and falling, the current environment bears little resemblance to the high-inflation, high-unemployment era.

Speaking overnight, Goolsbee emphasized that today’s economic fundamentals are far stronger, with inflation far below double digits and labor markets still tight.

However, he cautioned that simultaneous deterioration in both inflation and employment remains possible. “There’s definitely the possibility of both things getting worse at the same time,” he said. Goolsbee framed the outlook in terms of evaluating how large and lasting each side’s deviation might be—whether shocks are temporary or structural.

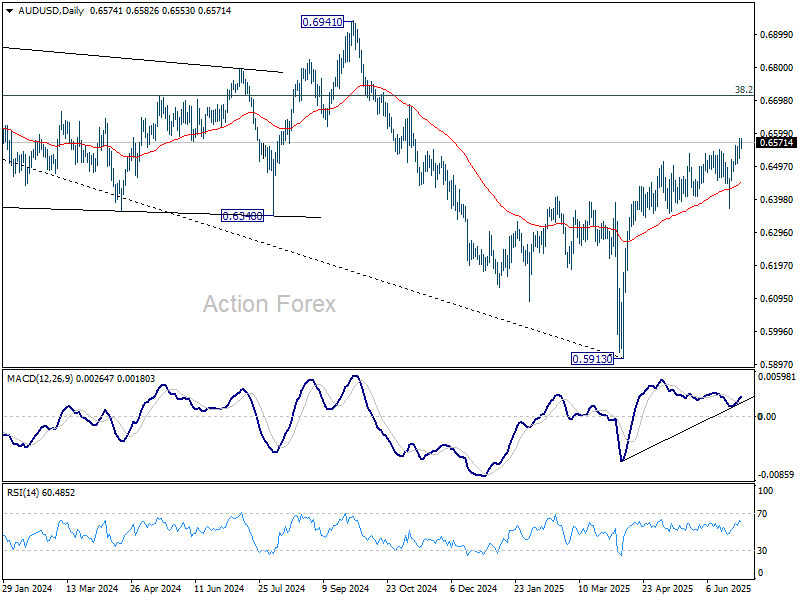

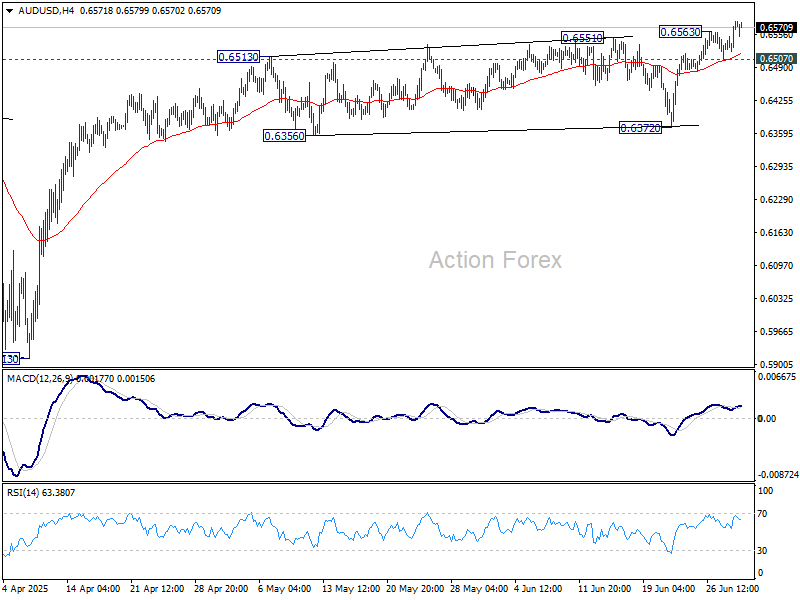

AUD/USD Daily Report

Daily Pivots: (S1) 0.6542; (P) 0.6563; (R1) 0.6603; More...

AUD/USD’s rally resumed after brief consolidations and intraday bias is back on the upside. Current rise from 0.5913 should target 0.6713 fibonacci level. On the downside, below 0.6507 will turn intraday bias neutral again. But outlook will remain bullish as long as 0.6372 support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).