Asian Sentiment Split As Japan And Korea Surge, China Lags On Weak PMI

Risk sentiment was mixed across Asian markets today, with Japan and South Korea extending record-breaking rallies while Chinese and Hong Kong stocks to underperformed. Nikkei 225 surged past the 52,000 mark for the first time, driven by strong momentum in the technology sector. Gains were led by heavyweight semiconductor and AI-related firms, buoyed by robust overnight earnings from Amazon and Apple in the U.S.

The latest Tokyo CPI data showed renewed upward pressure on prices, bringing the BoJ a step closer to another rate hike. Yet, for now, investors appear undeterred by the prospect of higher borrowing costs, viewing the data as confirmation of Japan’s improving growth dynamics rather than a policy risk.

South Korea’s KOSPI also hit new record highs, powered by relief in the trade sector following this week’s U.S.–Korea tariff agreement. The deal will see Washington lower auto tariffs on South Korean imports from 25% to 15%, in exchange for a USD 350B Korean investment package in the U.S. The agreement was hailed as a major win for Seoul’s export-heavy economy, with vehicles—comprising roughly one-third of South Korea’s shipments to the U.S.—expected to benefit most.

By contrast, China and Hong Kong markets lagged, with investors cautious following weak PMI manufacturing data showing continued contraction in factory activity. The data reinforced concerns that the Chinese economy remains under strain from the trade war and subdued domestic demand. At the same time, the Trump–Xi tariff truce, while easing immediate tensions, also reduces the urgency for Beijing to deliver more stimulus, leading investors to temper expectations for fresh policy easing.

In the currency markets, activity was quieter after a volatile week. Aussie continues to outperform, supported by resilient inflation data and strong risk sentiment. Loonie and Dollar follow closely behind, while Sterling remains at the bottom amid U.K. fiscal worries. Swiss Franc and Yen are also weaker as safe-haven demand fades. Euro and Kiwi sit in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 1.95%. Hong Kong HSI is down -0.81%. China Shanghai SSE is down -0.67%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is up 0.01 at 1.657. Overnight, DOW fell -0.23%. S&P 500 fell -0.99%. NASDAQ fell -1.57%. 10-year yield rose 0.035 to 4.093.

Japan’s Tokyo core CPI surges to 2.8%, BoJ hike timing still unclear

Japan’s Tokyo CPI figures for October showed broad-based acceleration in inflation, adding to pressure on the BoJ but stopping short of forcing an immediate policy move. Core CPI (excluding fresh food) climbed from 2.5% to 2.8% yoy, beating expectations of 2.6%. Core-core measure (excluding fresh food and energy) matched that rise, also hitting 2.8%, while headline inflation accelerated from 2.5% to 2.8%.

The increase was driven partly by a 38.4% surge in rice prices and the expiration of water-fee subsidies, which lifted utility costs. Food inflation, excluding fresh items, remained high at 6.7%, though slightly slower than September’s 6.9%. Meanwhile, services inflation was relatively steady at 1.6%, well below the 4.1% gain in goods prices. The mix suggests cost pressures are persistent but not yet translating into sustained demand-led inflation.

At its meeting yesterday, the BoJ left the policy rate unchanged at 0.50%. Governor Kazuo Ueda said the likelihood of the Bank’s baseline projection materializing had “heightened somewhat,” but reiterated that the BoJ wants to await “a bit more data” before considering another rate hike. He emphasized the need to observe whether firms continue to raise wages in response to higher U.S. tariffs before committing to further tightening. Overall, the latest inflation data and BoJ remarks reinforce expectations that the next rate hike remains a coin toss between December and January.

Japan’s industrial production rises 2.2% mom in September, indecisive fluctuation continues

Japan’s industrial production rose 2.2% mom in September, beating expectations of 1.6% and marking the first increase in three months. However, the Ministry of Economy, Trade and Industry kept its assessment unchanged, describing output as “fluctuating indecisively,” highlighting that the recovery remains fragile.

According to METI’s survey, manufacturers expect production to grow 1.9% mom in October but shrink -0.9% in November, pointing to continued short-term volatility.

Gains in September were broad-based, with 13 of 15 industrial sectors expanding. Notably, production machinery output surged 6.2% mom, driven by strong shipments of semiconductor manufacturing equipment to China and Taiwan. In contrast, transport equipment (excluding motor vehicles) and steel and non-ferrous metals recorded modest declines.

Meanwhile, retail sales rose 0.5% yoy, missing expectations of 0.7%, reflecting soft consumer demand despite improving wage and price trends.

China NBS Manufacturing PMI falls to 49 in October, contraction deepens

China’s official manufacturing PMI fell from 49.8 to 49.0 in October, missing expectations of 49.7 and marking the lowest reading in six months. The sector has now been in contraction since April. The new orders index dropped to 48.8 from 49.7, while the production sub-index declined sharply to 49.7 from 51.9, pointing to a broad slowdown in both output and demand.

NBS chief statistician Huo Lihui attributed the weaker reading to “the early release of some demand before the National Day holiday” and a “more complex international environment” that continues to weigh on activity.

Outside the factory sector, Non-Manufacturing PMI edged up slightly to 50.1 from 50.0, though it also missed forecasts of 50.2. As a result, the Composite PMI, which combines manufacturing and services, slipped to 50.0 from 50.6.

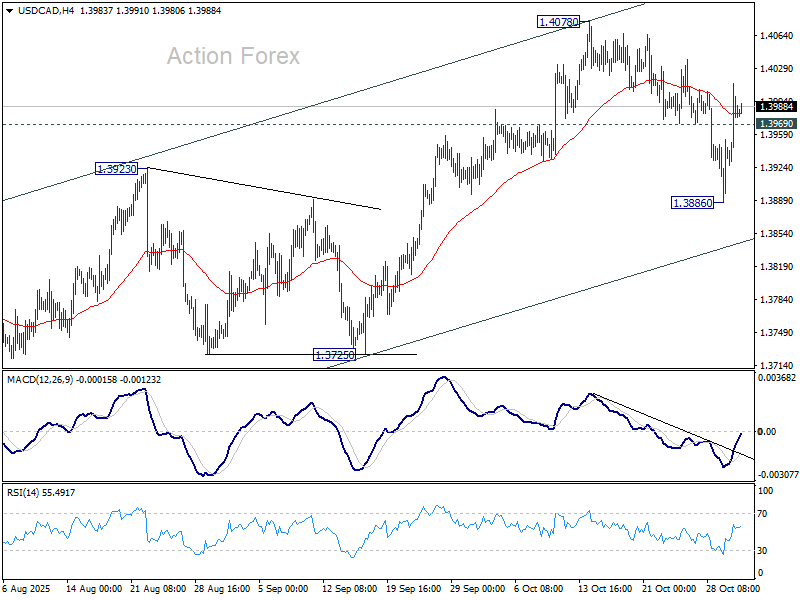

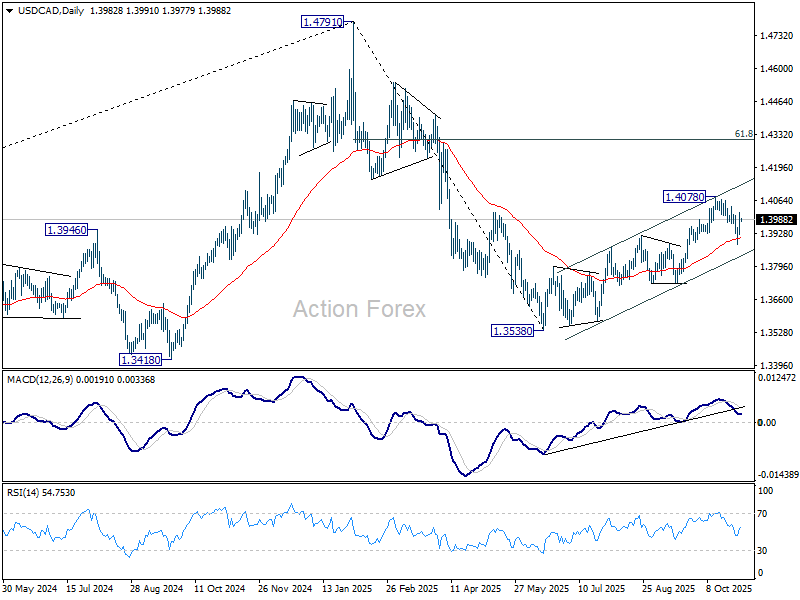

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3937; (P) 1.3975; (R1) 1.4024; More…

USD/CAD’s strong rebound suggests that pullback from 1.4078 has completed at 1.3886. That also keeps the rally from 1.3538 intact. Intraday bias is back on the upside for retesting 1.4078 resistance first. On the downside, though, break of 1.3886 will resume the fall to rising channel support (now at 1.3845).

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.

Gyrostat Capital Management: The Missing Allocation In Retirement Portfolio Construction?

For decades, retirement portfolios have largely been constructed using combinations of growth assets a... Read more

When The Gate Comes Down

A Stress Test Rather Than a ScandalApollo Debt Solutions is not a blow-up story. It is something arguably more instructi... Read more

What If The Investment Industry Is Benchmarking The Wrong Things?

Investment management is built around benchmarking. Fund managers compare themselves a... Read more

SpaceX Is Looks To Make History

The Biggest Bet in Wall Street History: SpaceX's $1.78 Trillion IPOThere are moments in financial history that stop you ... Read more

Gyrostat June Market Outlook: When Low Volatility Conceals Structural Risk

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direc... Read more

Why Low Volatility Is Not The Same As Low Risk

Why Low Volatility is Not The Same As Low Risk Some of the worst-performing portfolios in... Read more