The sharp interest rate rises expected to follow the collapse in the value of the pound do not bode well for the real estate sector in the UK.

Many of the REITs were already trading on large discounts to net asset value (NAV), in part due to the expected impact of rising interest rates on real estate values. Discounts have widened further in the past week as the pound weakened after chancellor Kwasi Kwarteng's Mini Budget - raising the prospect of a faster and higher rise in interest rates by the Bank of England, and a deeper recession that could potentially affect demand for space by tenants.

The Bank of England raised interest rates by 50 basis points last week, and there was an expectation it could hold an emergency meeting as early as this week which would see rates rise by an additional 75 to 100 basis points.

Concerns caused shares in all UK companies to fall, with real estate particularly hard hit. The EPRA UK REIT index fell 8% between Thursday (22 September) and Monday (26 September).

The Big Question: Asset allocation and the UK

Some REITs have been scrambling around to fix the rate on their debt to protect earnings being eroded by increasing interest costs. Real estate values are certain to fall as the higher cost of borrowing is factored into investors' return projections.

With UK government bonds currently at a 4.6% yield, investors will baulk at the yield on offer in some real estate sectors, like logistics where yields on prime assets had been reported to have fallen below 3.5%.

A softening of yields and capital values is inevitable then. The pass-through from interest rates to property yields will not be one-for-one, with the latter being less volatile. However, if REITs are to make strong returns over the next few years, they are going to have to do it the old-fashioned way - by delivering material income growth. The prospects for rental growth are heightened in sectors that operate in genuinely supply constrained markets.

The logistics market still has highly favourable supply and demand characteristics, despite Amazon's assertion that its warehouse expansion drive is over. Half-year take-up of logistics space reached a new record of 28.6m sq ft (surpassing last year's half-year total of 24.5m sq ft). Online retail accounted for 18% of the total (down from 35% last year) demonstrating that the market is not reliant on the boom in e-commerce. There has been a resurgence in demand from the manufacturing and automotive sectors, as supply chain resilience and the need to hold more inventory becomes more important.

Looking forward, there is a further 19.4m sq ft of space under offer, according to CBRE and 200m sq ft of longer-term occupier requirements logged by Savills.

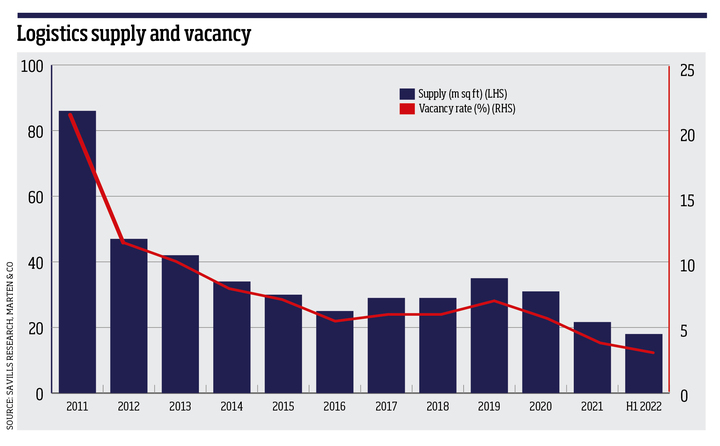

Compare this to the supply of warehouse space and the numbers get very interesting. There is just 18.4m sq ft of available space, according to Savills, and CBRE estimates that ready to occupy space remains at historically low levels of just 1.2%.

A large portion of the under-offer space will be on pre-let new builds, but even so the supply and demand dynamics are very favourable for continued rental growth.

As the economy hits the rocks, construction of new buildings will grind to a halt. Savills is tracking 16.5m sq ft of speculative development due for delivery in 2022 and 2023 and given the wider economic context new announcements are expected to tail off.

Treasury Committee calls for OBR forecast to be expedited due to 'continued market uncertainty'

The urban logistics, ‘last-mile' sub-sector has an even more of an acute supply and demand dynamic. For the first time the majority of warehouse lettings in the first half of this year was for ‘mid-box' logistics units (between 100,000 and 300,000 sq ft), while constraints on supply are severe.

The nature of urban logistics, being located close to large towns and cities, make gaining planning for this use class very difficult. In addition, rising construction costs, as well as land values, has rendered new build projects pointless given that the cost of building an urban logistics scheme exceeds the current values of a built property.

Strong earnings growth among the listed logistics specialists will not be reciprocated in the NAV growth we have become accustomed to in recent years. However, as a long-term income investment, logistics-focused REITs look attractive.

The market leader SEGRO was trading on a discount to NAV of 39% (at 26 September), while Tritax Big Box REIT was on a 44% discount. Meanwhile, Urban Logistics REIT, the only company purely focused on that end of the sector, was trading on a 28% discount. These companies have a proven track record of growing rents through intensive asset management, whether they can do it during economic turbulence will be key.

We are certainly going to see the wheat separated from the chaff over the next few years. These three logistics funds are in a great position - with genuine supply constraints supporting income growth and strong management teams to extract it - to prove themselves when the chips are down.

Richard Williams is a property analyst at QuotedData