The intelligence layer for fintech professionals who think for themselves.

Primary source intelligence. Original analysis. Contributed pieces from the people defining the industry.

Trusted by professionals at JP Morgan, Coinbase, BlackRock, Klarna and more.

Join the FinTech Weekly Clarity Circle →

Insights from 6M Credit Applications: How Digital Credit Score Correlates with Defaults

As digital interactions shape how people manage their finances, lenders are paying closer attention to alternative data.

Risk teams now use credit scoring software to surface risk signals that traditional credit bureaus often miss, especially for underserved and thin-file borrowers.

But a critical question remains: do these digital signals actually translate into real-world credit outcomes?

This article presents key findings from a large-scale research project conducted by RiskSeal, analyzing more than 6 million lending decisions.

Testing digital credit scoring in a real market

Each application in the study was scored using only the data available at the time of submission, mirroring how underwriting decisions are made in practice.

Across both emerging and developed markets, lenders face a similar challenge: parts of the borrower population remain invisible (or only partially visible) to credit bureaus.

In emerging markets, this is often due to limited bureau penetration. In more mature markets, it stems from thin-file segments such as younger borrowers, migrants, or digitally native consumers.

To capture a broad range of lending environments, RiskSeal partnered with seven institutions, including microfinance providers, buy-now-pay-later platforms, and a neobank.

How the analysis was conducted

The analysis examined over 6.1 million loan applications. Each application was scored in real time, using only data available at the moment of submission, mirroring live underwriting conditions.

Defaults were defined consistently as payments 90 days or more past due. Applicants were grouped into score bands, and default rates were measured across those bands.

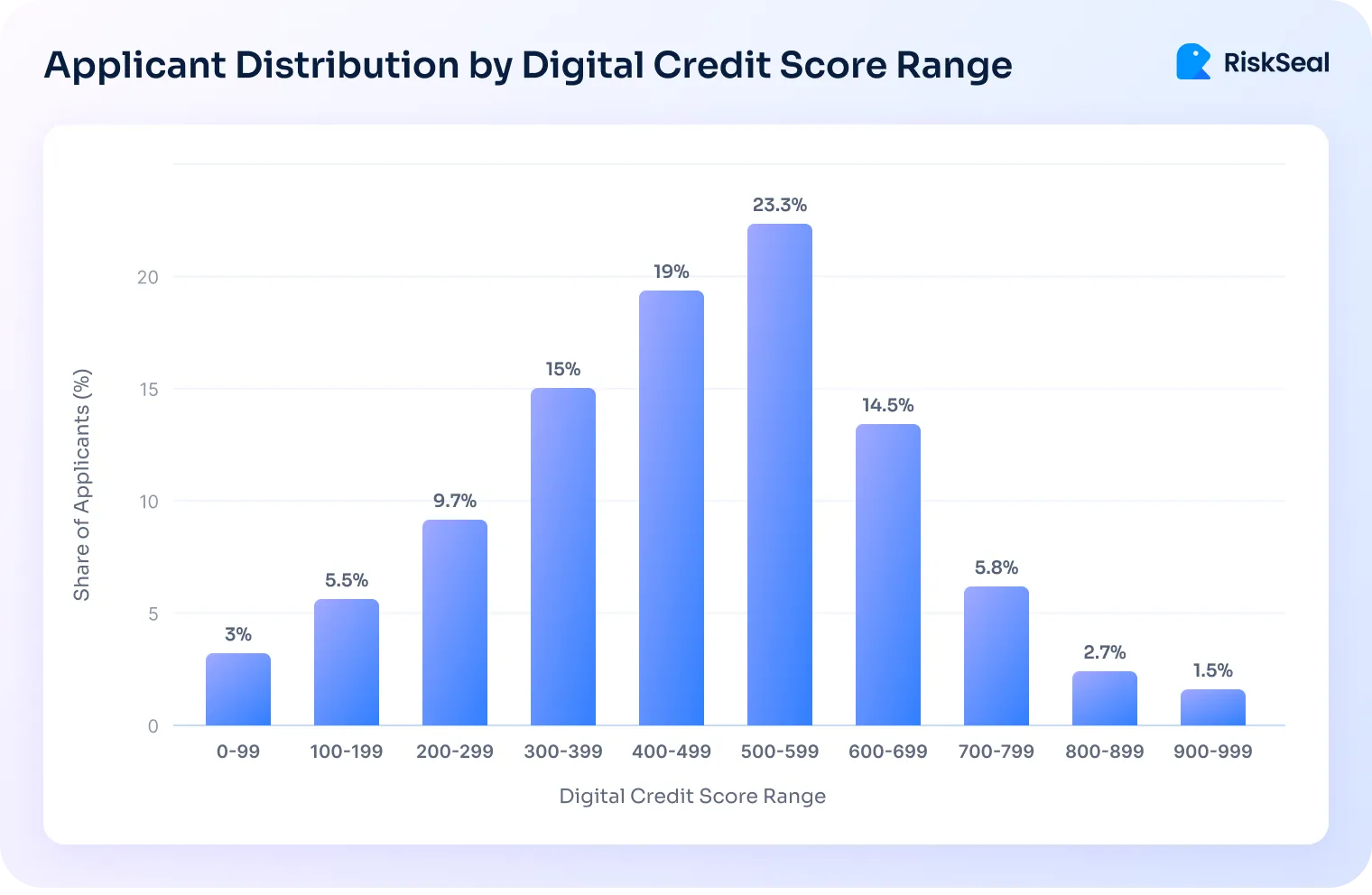

Where borrowers fall on the digital score spectrum

The researchers analyzed how applicants were distributed across the digital score range.

This step is critical because heavily populated score bands have a disproportionate impact on portfolio risk and underwriting outcomes.

Borrowers were not evenly distributed across score ranges:

- Low scores (0–299): 18.2% of applicants

- Mid-range scores (300–599): 57.3% of applicants

- High scores (600–999): 24.5% of applicants

The mid-range borrowers are often the most difficult to assess using credit bureau data alone. They are neither clearly high-risk nor clearly low-risk.

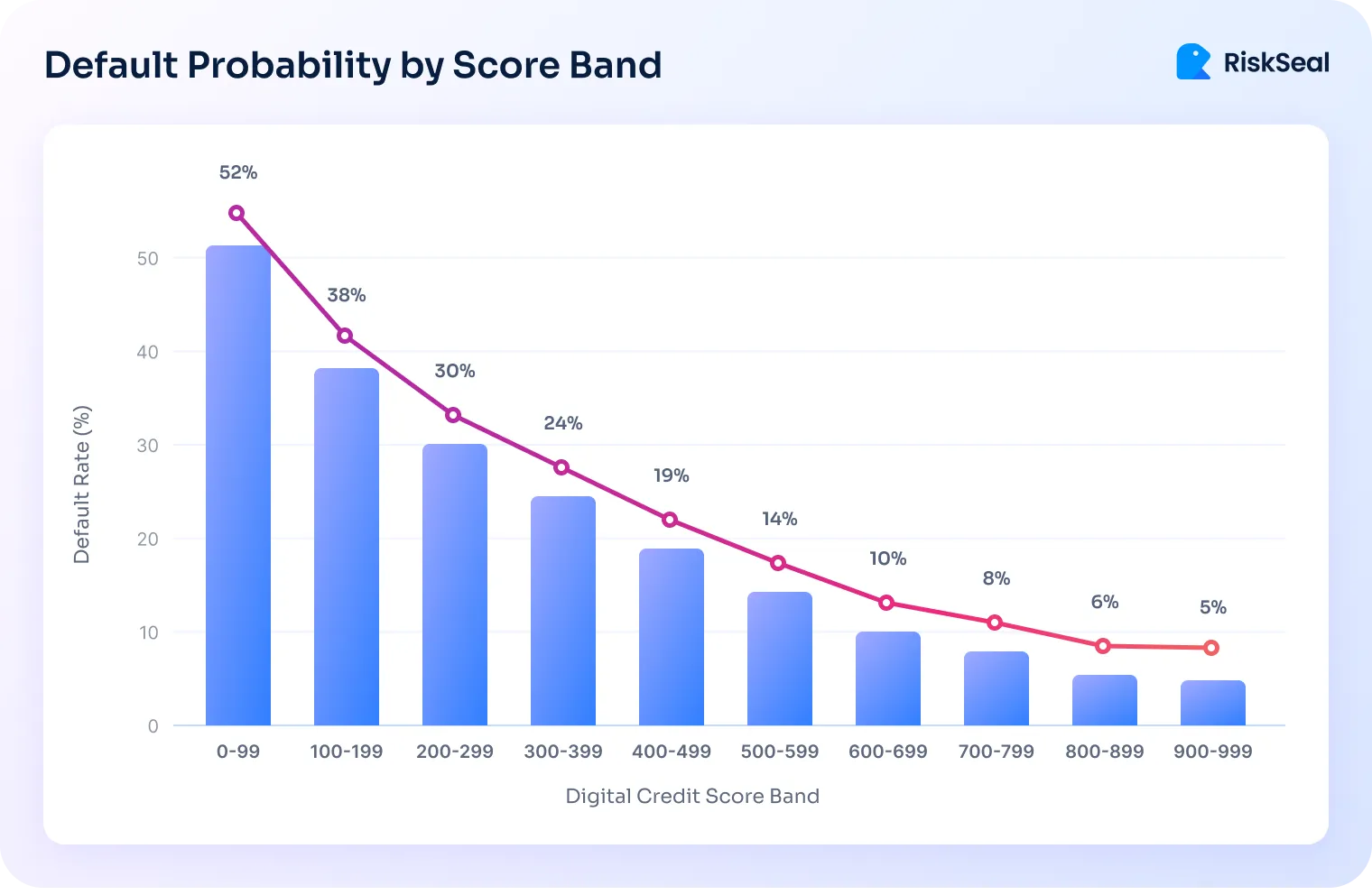

The core finding: default rates fall as scores rise

The analysis shows a clear, monotonic relationship between digital credit scores and default risk: as scores increase, default rates consistently decline.

At the bottom of the scale, more than half of borrowers defaulted. Among top scorers, defaults dropped to single digits.

The mid-range tells the most important story. As scores moved through the middle bands, default rates fell steadily from the high twenties to the mid-teens.

This demonstrates meaningful risk differentiation exactly where lenders need it most.

What the digital credit score is actually capturing

A digital credit score looks at patterns in a borrower’s digital footprint to estimate stability, authenticity, and risk.

It does not judge people based on one “red flag.” Instead, it combines multiple small signals and reads them in context.

A digital credit score typically captures signals like:

- How established the identity looks, such as long-lived email addresses and phone numbers with multi-year activity.

- Whether the digital identity is consistent, like matching names and details across email, apps, and online profiles.

- Device and network stability, including consistent device usage and low-variance IP patterns over time.

- Recurring financial behavior, such as active paid subscriptions that renew regularly.

- Real-world purchase activity, including e-commerce transactions on established accounts.

- Long-term messaging platform use, for example stable activity on WhatsApp or Telegram.

- Clear signs of fraud or manipulation, like disposable contact details, virtual numbers linked to fraud, and anonymized or rapidly shifting IPs, etc.

Some digital behaviors require even more careful interpretation.

VPN usage, prepaid vs. postpaid plans, low social presence, number portability, or device resets are often neutral on their own.

They become meaningful only when paired with timing, frequency, and other supporting signals.

Each signal on its own may be weak. But when several of them point in the same direction, the score becomes a strong indicator of repayment risk and fraud exposure.

What this means for risk teams

Rather than replacing bureau data, digital scoring strengthens it.

Risk teams can now fill information gaps and sharpen risk differentiation where underwriting decisions are the hardest.

Particularly, in the large middle segment of borrowers who fall outside traditional approval or decline thresholds.

This approach enables more confident credit expansion without loosening risk discipline.

Teams can approve more applicants in the mid range by relying on current behavior rather than conservative assumptions. The result is portfolio growth with improved risk performance.